Table Of Content

- Additional Liability Insurance with an Umbrella Policy

- How Bankrate chose the best home insurance companies in California

- Fewer carriers willing to write policies in high-risk states

- Get a home insurance quote customized to your needs

- What affects my homeowners insurance rate?

- Factors Used to Calculate Home Insurance Rates

One-third of those who lost coverage moved or plan to move as a result of that, they told RedFin. The California Geological Survey notes that there are usually two to three earthquakes big enough to cause moderate structural damage each year. Compare rates from participating carriers in your area via EverQuote's website. Beck Andrew Salgado covers trending topics in the Austin business ecosystem for the American-Statesman. Meanwhile, the consistent threat of hurricanes and tropical storms is causing some insurers to pull out of coastal states altogether. Government data show that 2023 was a record-breaking year for damaging weather and climate events.

Additional Liability Insurance with an Umbrella Policy

The first quote has a lower dwelling limit, but a higher liability limit and a slightly higher deductible than the second quote. If you file a claim for damage to your home, you’ll have to pay $1,500 out of pocket — your deductible limit — if you purchase the first quote, and only $1,000 if you purchase the second quote. Just because something is excluded from your home insurance policy does not mean you can’t be covered for it, though. Home insurance providers sell separate endorsements for earthquakes, floods and other perils to protect your home further. Jessa Claeys is an insurance editor for Bankrate with over a decade of experience writing, editing and leading teams of content creators. She currently covers auto, home and life insurance with the goal of helping others secure a healthy financial future.

How Bankrate chose the best home insurance companies in California

The dwelling insurance limit should cover the cost of rebuilding your house. Get Forbes Advisor’s ratings of the best insurance companies and helpful information on how to find the best travel, auto, home, health, life, pet, and small business coverage for your needs. Bundling insurance means you buy both your home and auto insurance policies from the same company.

Best Homeowners Insurance for Older Homes of 2024 - MarketWatch

Best Homeowners Insurance for Older Homes of 2024.

Posted: Mon, 22 Apr 2024 07:00:00 GMT [source]

Fewer carriers willing to write policies in high-risk states

All rates based on the above coverage limits except where otherwise noted. You’ll pay more for higher limits, but the extra coverage will give you more financial protection if disaster strikes. When analyzing costs for different coverage levels and risk factors, we changed just one variable at a time to ensure the rates we’re comparing are fair and representative of the factor at hand. We've seen this trend continue on in high-risk states like Florida and California. Here's the average annual premium for a homeowner with a clean claims history versus a homeowner with one, three, or five claims on their record. Given the increased risk of damage and claims, you'll generally have to pay more for home insurance as your home ages.

Get a home insurance quote customized to your needs

This is because credit history can be an indicator of risk — studies show that those with lower credit scores tend to file more claims compared to those with higher credit scores. As a result, home insurance for people with bad credit is generally more expensive compared to those with average, good and excellent credit scores. If you own your home with a partner, their credit history may also impact your rates.

What affects my homeowners insurance rate?

Best Homeowners Insurance in Georgia of 2024 - MarketWatch

Best Homeowners Insurance in Georgia of 2024.

Posted: Mon, 22 Apr 2024 07:00:00 GMT [source]

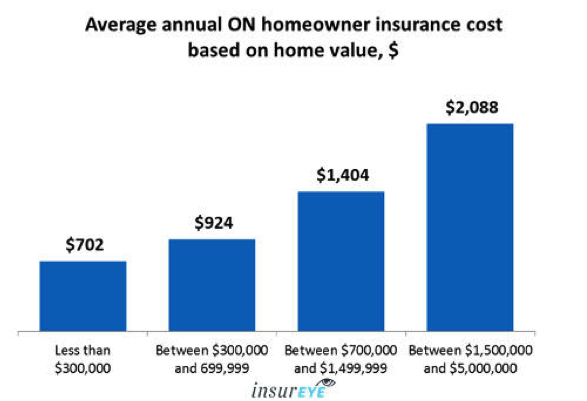

Condo insurance is similar to home insurance in that it covers repairs to the interior of your condo unit, your personal belongings, liability, medical payments to others and additional living expenses. The exterior of the building is covered by the homeowner association’s master policy. Yes, it’s worth your time to compare quotes even if you already have homeowners insurance. If you don’t, you could be missing out on savings for similar coverage with another insurance company. Among the home insurance companies we analyzed, average rates show a cost increase of 32% from $350,000 to $500,000 in dwelling coverage and a 41% cost increase going from $500,000 to $750,000 in coverage.

Coverage and cost vary drastically based on several unique factors, including the age of a home, square footage, cost of building materials and location. Each state has different regulations and natural hazards that also impact the cost of home insurance. Plus, if you have a loan on your home, your financial lender can also have a say in the minimum amount of home insurance coverage you must purchase. While home insurance policies include several other coverages that protect everything from your personal belongings to liability, dwelling coverage has by far the biggest impact on your insurance premiums. There are several online calculators that you can use to calculate your dwelling coverage limit, but most insurers should be able to provide you with an estimate when you get a quote.

Does getting a homeowners insurance quote affect your credit score?

You also want to make sure your dwelling coverage amount matches the cost to rebuild your home with equitable materials, and that you have enough liability insurance to protect your savings and assets if you are sued. Each insurer has its own formula for calculating quotes, which is why it’s advantageous to compare home insurance quotes from multiple companies. If you skip this crucial step, you could miss out on significant savings. We made minor changes to the sample policy in cases where rates for the above coverage limits or deductibles weren’t available. Homeowners insurance policies typically include six standard types of coverage. Homeowners insurance costs an average of $1,915 a year, or about $160 a month, according to NerdWallet’s analysis.

We assessed the average rates, coverage options, discounts, third-party scores and ratings, and digital tools of California home insurance companies to find the options that stand out. ZIP code in Honolulu, Hawaii, has the lowest average homeowners insurance cost in the nation, but dozens of other Hawaii ZIP codes are also among the cheapest in the country. One factor is that standard home policies in Hawaii do not cover hurricane damage. Ever since Hurricane Iniki in 1992, homeowners in Hawaii must buy separate hurricane damage policies, per Michael Barry, chief communications officer of the Insurance Information Institute (III). The more claims insurers pay out for damage caused by wind, hail, and rain, the higher homeowners insurance costs will be for everyone.

You should also consider whether you want replacement cost on your belongings or actual cash value, which factors in depreciation. And with an average premium of $1,650 per year, you can expect your Allstate insurance home quote estimate to hover right around the national average. Our proprietary rating methodology takes multiple factors into account, including customer satisfaction, cost, financial strength, and policy offerings.

Personal property coverage is generally set at 50% to 70% of your dwelling limit. That means that if your dwelling coverage is $500,000 and your personal property coverage is set at 50%, your personal property limit would be $250,000. Completing a home inventory will help you determine your coverage needs. Before panic-buying every home insurance endorsement your insurer offers, it’s helpful to first understand which disasters are specifically covered in your policy. Once you have a better understanding of what’s covered by your home insurance policy, you can identify potential coverage gaps and purchase more coverage if you need it. If you’re wondering why California’s home insurance rates are so low considering how risky the state is, it’s largely because of strict consumer protection laws.

No comments:

Post a Comment